-

Setting the Record Straight on JetBlue’s Antitrust Arguments

المصدر: Nasdaq GlobeNewswire / 28 يونيو 2022 06:45:00 America/New_York

JetBlue’s “Less Seats, Higher Prices” Acquisition Is a Dead End

JetBlue’s Misdirection and Negative Attacks Cannot Hide the Fatal Flaws With its Bid to Eliminate Spirit and Derail the Frontier/Spirit Procompetitive Merger

As Opposed to JetBlue’s Illusory Bid, a Frontier Merger Offers Significant Upside

DENVER, June 28, 2022 (GLOBE NEWSWIRE) -- Frontier Group Holdings, Inc. (“Frontier”) (NASDAQ: ULCC), parent company of Frontier Airlines, Inc., today issued the following statement regarding Frontier’s proposed merger with Spirit.

Over the last few weeks, JetBlue has proclaimed that Spirit management is hiding behind “false” and “misleading” antitrust concerns so as to deny JetBlue the right to take over—and erase from existence—the nation’s largest ultra-low cost carrier.

JetBlue is not telling you the truth. A Spirit acquisition by JetBlue would lead to a dead end—a fact that no amount of money, bluster, or misdirection will change. And the only value Spirit stockholders would be likely to receive from JetBlue’s proposal is the reverse termination fee, because JetBlue’s proposal lacks any realistic likelihood of obtaining regulatory approval.

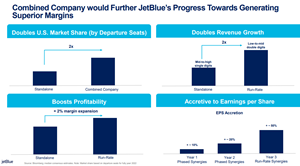

JetBlue admitted that it will permanently remove capacity from the market by retrofitting Spirit’s fleet to remove seats. Antitrust lawyers call that an “output restriction,” and it is fatal to JetBlue’s bid. So are JetBlue’s admitted price increases. Less airline capacity means higher fares. JetBlue’s CEO, Robin Hayes, certainly knows that. He observed just a few days ago, “The average price of air fares will go up because there is [sic] less seats.”1 That is exactly what JetBlue would do with Spirit’s fleet. Indeed, in announcing its bid on April 6, JetBlue said that the acquisition would increase its profit margins, despite higher costs.

These facts—admitted higher prices and lower output—guarantee that JetBlue could never secure clearance for its proposed acquisition of Spirit. No claimed “divestitures” of airport slots or gates, or false claims or gimmicks, can fix JetBlue’s fatal problems.

And these are not even JetBlue’s only regulatory problems. The anticompetitive rationale for its bid is obvious. JetBlue even admitted it, stating in its 2021 10-K that the Frontier/Spirit deal is a threat to JetBlue’s “competitiveness”—and an example of a merger that “could cause fares of our competitors to be reduced.” Mr. Hayes later conceded that “the timing” of JetBlue’s bid was “definitely driven by the announcement”2 of the proposed ULCC merger.

Then there is the U.S. Department of Justice’s pending lawsuit against JetBlue to block its Northeast Alliance with American Airlines. Despite assuring everyone—including Spirit shareholders—that a transaction would spread the mythical, so-called “JetBlue Effect,” Mr. Hayes previously admitted the DOJ’s reason for bringing the NEA lawsuit: “DOJ believes that American’s influence will bring an end to the “JetBlue Effect.”3 The DOJ has therefore already disputed JetBlue’s arguments for a transaction. And, contrary to Mr. Hayes’ assertion that the NEA litigation will be resolved shortly—and thus will have no effect either way on the JetBlue/Spirit acquisition—it will surely take years to resolve the NEA litigation, through trial and all inevitable appeals. While Spirit shareholders wait for what, exactly? A break-up fee, years later, out of the illusory JetBlue bid?

For weeks, JetBlue has filled the airwaves with noise. It has shared an astonishing array of misleading claims, all while ignoring obvious and lethal antitrust problems. Indeed, just yesterday, JetBlue claimed that “outside experts agree that, within the current administration, our transaction has a similar chance as Frontier in gaining approval.”4 JetBlue includes no source, of course—so the “outside experts” it appears to be talking about? Its very own, JetBlue-hired antitrust lawyer.

JetBlue wants you to think that Frontier and JetBlue bring antitrust risk profiles that differ only in degree, not in kind. But nothing could be further from the truth. A JetBlue acquisition of Spirit could not succeed.

A Frontier/Spirit merger is entirely different. Our transaction will increase output and reduce prices by bringing ultra-low fares to more routes in competition with larger, higher cost, higher fare airlines. A combined Frontier and Spirit will stimulate demand by inducing people to fly when the high fares offered by JetBlue and the Big Four would otherwise price them out of the market.

Context: the evolution of JetBlue’s antitrust arguments

JetBlue’s antitrust-related arguments initially sputtered. Observers commonly noted that

- DOJ was already in federal court accusing JetBlue of being an antitrust violator, and

- The Frontier/Spirit combination had obvious synergies and a procompetitive narrative that the “headscratcher” JetBlue/Spirit bid conspicuously lacked.

But as its arguments went unheeded, JetBlue shifted course. Its attacks grew negative and went low. JetBlue prepared numerous materials aimed at muddling the antitrust landscape. It built its own web site, filled with attacks on Spirit and the Spirit/Frontier deal. It even choreographed a Q&A video about antitrust, featuring yet another JetBlue-hired lawyer—this one labeled as an “antitrust expert” because, well, “JetBlue-retained antitrust lawyer” lacks the same appearance of impartiality. And it spared no expense. The Q&A video with JetBlue’s antitrust lawyer, according to its “Final Edit10.mp4” title, apparently took at least 10 takes or versions to deliver the desired message:5

Spin, as it turns out, is hard to get just right.

Perhaps most troublingly, JetBlue resorted to attacking the integrity of both Spirit and Frontier—and anyone else who disagrees with JetBlue’s vision of the world. It has falsely attacked Spirit’s board of directors via a thesaurus-rich tapestry of pejoratives: “Entrenched…stonewalling…deeply conflicted…strikingly poor…astounding failure;” the list goes on. And it also unloaded on Glass Lewis—a prominent independent proxy advisor— as having allegedly conducted a “remarkably superficial regulatory analysis,”6 because Glass Lewis concluded that the Frontier/Spirit deal was, in fact, in Spirit shareholders’ best interest.

There is an old saying about those who doth protest too much.

JetBlue has no answer to its first glaring antitrust problem:

an admitted, immediate and substantial output reduction upon closing of the Spirit acquisitionAntitrust law asks whether a merger is likely to substantially lessen competition. Of the key focal points of this analysis, the most prominent are the effects on output and prices. A JetBlue/Spirit combination would be doomed from the outset because JetBlue has already admitted that the acquisition would reduce capacity (output) and increase fares (prices).

JetBlue knows this. In the NEA litigation, JetBlue tried to get the DOJ’s antitrust claims thrown out for want of allegations that the alliance would reduce output or increase prices, arguing:

“The Complaint is defective as a matter of law because Plaintiffs have not alleged that the NEA has actually harmed competition. The NEA has been underway for nine months, yet Plaintiffs do not allege that it has caused a single higher price, any reduction in quality or the slightest reduction in output…”7

The court recently rejected JetBlue’s arguments, finding that the DOJ had indeed alleged more than enough facts to plausibly state an antitrust violation.

Here, by contrast, JetBlue has already admitted that reduced output and increased prices are the very point and rationale of its proposed acquisition of Spirit. At the very first investor presentation, Mr. Hayes admitted that JetBlue will reconfigure Spirit’s aircraft to remove 10-15% of seat capacity. Reports were not kind:

“Indeed, there was a tone of mild incredulity during the investor conference call. ‘I’m just trying to square away how removing seats right now is pro-consumer over the long haul,’ Connor Cunningham of MKM Partners asked, referring to the removal of capacity from the market as Spirit’s dense A320 family aircraft get converted to JetBlue’s significantly less-dense configuration. . . . Even [] pro-consumer advocates would agree reducing capacity across Spirit’s entire fleet is only likely to put upward pressure on fares.”8

Even without other antitrust problems (and there are many), that admission marks the end of the road for JetBlue. But in all of its pro-acquisition propaganda, website, or choreographed videos, JetBlue never once addresses this fatal problem or even claims that it can. Nor does it ever dispute that the Frontier/Spirit merger will lead to the opposite—an increase in capacity, and, therefore, output due to the undisputed demand stimulation that ultra-low-fares fuel, the many new routes that a combined Frontier/Spirit could enter in competition with far-larger airlines, and the enhanced growth trajectory created by our merger, all creating a virtuous cycle of enhanced ULCC competition.

JetBlue has no answer to its second glaring antitrust problem:

an admitted, immediate and substantial price increase upon closing of the Spirit acquisitionAs JetBlue’s CEO observed on June 20, capacity reductions mean higher fares.9 Tellingly, in its April 6 investor presentation, JetBlue assured investors that, despite cost increases, its acquisition of Spirit would lead to significantly higher margins:10

As a matter of math, that means higher prices for passengers (a lot higher, given the difference between Spirit’s ultra-low fares and JetBlue’s average fares):

“Simply removing 10-15% of the seating capacity from Spirit’s operations will drive up unit costs. JetBlue CFO Ursula Hurley acknowledges this challenge. She notes that post-merger the airline hopes to maintain JetBlue’s existing cost levels, which are higher than Spirit’s. And there is no way JetBlue can deliver profitable operations on fewer total seats flying without raising the prices on those seats. . . . It will have to operate the legacy Spirit fleet at fares higher than what Spirit charges today. Plus, with a lower fare competitor eliminated JetBlue likely can afford to raise fares beyond what it charges today.”11

This is not surprising: the cost differential between JetBlue and Spirit is so significant that JetBlue would have no option other than a significant increase in fares.

The principal measure of structural cost differentials is CASM ex fuel (cost per available seat mile excluding fuel costs). By that metric, for 2021, JetBlue was roughly 50% higher than either Spirit or Frontier, as the following chart—drawn from the companies’ SEC filings—makes clear:

2019/2021 CASM ex Fuel (in cents)

Further, JetBlue has admitted that its base plan assumes bringing Spirit’s cost structure (CASM ex Fuel) up to JetBlue’s CASM following an acquisition. As JetBlue’s CFO stated:

“…, so in terms of the synergies, we provided a net number. So in regards to the dissynergies associated with labor and then you're correct, there's puts and takes in terms of the density. The base case assumes that the Spirit fleet is brought up to JetBlue density at this point in time. And with that, in terms of the overarching CASM ex-fuel base, we don't believe there will be a material change to the unit cost base compared to JetBlue today, given, to your point, the dissynergies and the puts and takes around density.”12

That means that JetBlue plans on increasing Spirit fares by approximately ~40% in order to cover the incremental cost structure and operate at existing JetBlue margins.

An admission of systemwide substantial price increases is a fatal antitrust problem for JetBlue. Once again, JetBlue has no answer. Nor does it ever dispute that the Frontier/Spirit merger will lead to the opposite: lower costs supporting continued ultra-low fares, far lower than Jet Blue’s, and far more of them given the capacity (output) expansion synergies and ultra-low-fare growth (lower prices) at the heart of the Frontier/Spirit merger.

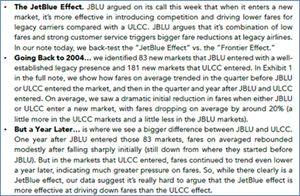

The “JetBlue Effect” is not a DOJ-blessed, get-out-of-jail card for JetBlue,

but another significant strike against JetBlue’s acquisition of SpiritJetBlue’s entire antitrust pitch to investors rests on the imagined superiority of the “JetBlue Effect” over the clearly more significant “ULCC Effect,” which has already forced legacy and other high-cost carriers like JetBlue to offer an entire new class of low fares. JetBlue can claim no equivalent pro-consumer impact, despite already having the size of a combined Frontier/Spirit. No ULCC in the United States has achieved the full competitive potential of the ultra-low-cost business model—none is at scale or adequately resourced. And, yet, the ULCC Effect has already disrupted the airline industry in a far more profound way than JetBlue can claim credit for.

Undeterred, and without disclosing any supporting data, JetBlue claims that its presence decreases legacy fares by ~16%. It argues that the DOJ itself has recognized and blessed the power of the JetBlue Effect (in the NEA litigation), and that JetBlue’s assimilation of Spirit is therefore procompetitive because it will increase the power and reach of this DOJ-blessed “JetBlue Effect.”

At a May 26, 2022 Wolfe Research conference, Mr. Hayes summed up his argument:

“I think that our conviction and our [confidence] on the regulatory side is really predicated, first of all, on the JetBlue effect, which is documented and proven. And if you don't take my word for it, take the Department of Justice's word for it because they now – in the complaint they filed against the NEA, they talked persuasively about the JetBlue effect and our disruptive impact on fares.13

This is classic misdirection. Yes, the DOJ mentions the “JetBlue Effect” in the NEA litigation complaint. But the DOJ’s actual allegation is that the NEA compromises JetBlue’s incentives to compete and the entire JetBlue Effect; in other words, the DOJ believes that there will be no JetBlue Effect with the NEA in place.

Mr. Hayes knows all this. He admitted it in September 2021, when he issued a press release the day the NEA litigation was filed:14

“DOJ believes that American’s influence will bring an end to the “JetBlue Effect.”

The same misdirection accompanies JetBlue’s many recent, preposterous statements that the NEA litigation does not impact the Spirit acquisition in the slightest. For example, here’s what JetBlue said just a few weeks ago:Spirit’s Suggestion that Our Northeast Alliance Is a Regulatory Obstacle Has No Basis in Fact or in Law. The Northeast Alliance litigation will go to trial this September, and we believe the outcome of that trial will not impact the outcome of the regulatory process for the acquisition of Spirit, which will likely take place later. If the court allows the DOJ to block the Northeast Alliance, by definition it will not be an obstacle to the acquisition of Spirit. If we are successful in defending the case, as we think we will be, it will be a testament that the alliance is procompetitive, disproving Spirit’s claim. In either case, the Northeast Alliance litigation does not impact JetBlue’s ability to acquire Spirit.15

And here’s what JetBlue told you just yesterday—and what it so very much wants you to believe:

“the litigation outcome [is] irrelevant… The Northeast Alliance trial will begin in September, and will be decided long before the resolution of any challenge to the Spirit transaction.”16

That is simply not accurate. It will take years to resolve the NEA litigation. Trial will occur later this year, in September…and then there will then be months of post-trial filings. The judge may issue an opinion months after that (or even longer). There will then inevitably be appeals, from one or more parties. Years of litigation. In fact, it is virtually certain that the NEA litigation will be outstanding without reaching a final resolution while at the same time JetBlue is likely also litigating with the DOJ over a Spirit transaction. But JetBlue does not want you to know any of this. The DOJ’s lawsuit alleging that the NEA compromises any historical “JetBlue Effect” is another big strike against a JetBlue/Spirit acquisition, not a reason for it.

JetBlue’s argument that the “JetBlue Effect” has historically been more significant in lowering fares than ultra-low-fares from Spirit and Frontier is a fantasy

Since announcing the proposed Spirit acquisition, JetBlue has claimed that the “JetBlue Effect” is greater than any effect that ultra-low-cost carriers have on lowering overall fares. This claim is not true, either.

Two independent groups looked at JetBlue’s “3x” claim and ran their own analyses…and debunked JetBlue’s statement. Wolfe Research analyzed it directly, and found it not to be true:17

J.P. Morgan looked at the claim as well, and raised another issue: JetBlue had failed to address the demand stimulation that is an essential and proven component of the ULCC business model worldwide. This demand stimulation would only get stronger and more sustainable under a Frontier/Spirit combination.18

In any event, the “JetBlue Effect is stronger” claim is nonsensical, contradicting what everyone knows about how airline industry pricing has shifted over the last few years directly as a result of ultra-low-fares.

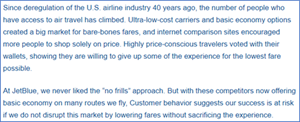

Despite wishing to charge high prices, JetBlue concedes that ULCC competition has forced it to reduce its own fares. In September 2018, JetBlue issued a letter from its President and Chief Operating Officer, Joanna Geraghty, explaining that ultra-low-fares (and the “basic economy” fares that legacies had been forced to respond with) stimulated great demand, revealing many customers who seek low fares, and that JetBlue felt forced to offer its own “basic” fares in response:19

That’s a dramatic admission. JetBlue agrees that ultra-low-cost airlines have transformed airline pricing, triggering an industry-wide ultra-low fare class in response. JetBlue concedes that it reluctantly lowered fares on account of ULCC-induced low prices—because it had to. The alternative would have been to lose passengers. And now, in an about-face, it insists that the “JetBlue Effect” somehow exerts greater downward pressure on industry pricing than the ULCC Effect (and more than the magnified ULCC Effect that a combined Frontier/Spirit would create). JetBlue’s own actions and statements belie that claim.Hundreds of articles and reports address this overall issue; here are just two:

- “JetBlue Airways announced it will now be adding its own edition of basic economy to its seating choices, joining domestic rivals American Airlines, United Airlines, and Delta Airlines in offering lower-priced economy fares.... Basic economy was created by America’s biggest three airlines—American, United, and Delta—as a reaction to lower fares offered by ultra-low-cost carriers like Spirit Airlines and Frontier Airlines. Basic economy seeks to allow larger airlines to remain competitive against those super-low fares others offer without sacrificing the revenue generated by their traditional economy-class seating prices.”20

- “Call it the Spirit Syndrome or the Wow Effect. More airlines are copying the stripped-down fare model of the minimalist airlines, offering lower fares for fewer perks. American, United and Delta have all introduced this fare option. Last week, JetBlue announced that it will add a basic pricing tier next year.”21

JetBlue’s own begrudging acceptance of lower fares shows that ultra-low-cost airlines have a far more profound effect on industry dynamics and pricing than any “JetBlue Effect” does. Indeed, the ULCC Effect has served to keep JetBlue’s fares lower than they otherwise would be. And that fact, of course, is yet another reason why JetBlue’s bid to acquire the largest ULCC will never obtain antitrust approval.

Airline competitors would rather see JetBlue acquire Spirit

In its latest June 7 presentation deck, extolling the virtues of the JetBlue acquisition (this one 41-pages long), JetBlue included a slide meant to indicate that “independent industry observers” saw the two deals as similar. Here’s in part what it said there: 22

This is remarkable. Scott Kirby is not an “independent industry observer”—he is the CEO of United Airlines, which is an extremely interested party in whether a ULCC is acquired and extinguished—as JetBlue seeks to do—or becomes a bigger and stronger ULCC, better able to penetrate and disrupt pricing in United-dominated routes (as Frontier and Spirit together would do).

The CEO of one of the biggest legacy airlines, publicly undermining the Frontier/Spirit deal, shows which transaction is procompetitive, will hurt legacies and force them to lower fares.

JetBlue’s personal attacks against the DOJ,

and anyone else who dares disagree, do not further JetBlue’s standingAs you have seen, JetBlue goes on the personal attack—and hits low—when its audience questions or refutes its claims. The Spirit board has real issues with JetBlue’s bid? Go after them personally, accusing them of being conflicted, biased, and not doing their jobs. Glass Lewis is not buying the yarn JetBlue is trying to sell? Claim that they don’t know how to do their jobs, or are deliberately ignoring facts, in conducting their “remarkably superficial regulatory analysis.” Frontier maintains and strengthens its bid—the only one that can realistically pass antitrust review? Claim that chummy ties with the Spirit board explain it all.

And it is worth highlighting just how far JetBlue is willing to take this approach: all the way to the Department of Justice itself, the agency responsible for reviewing a JetBlue/Spirit combination. The day DOJ filed its NEA lawsuit, Mr. Hayes issued a detailed press release assailing DOJ as:23

“Hypocritical”

“Standing in the way of JetBlue’s growth”

“Using the public’s resources to stifle competition”

“The irony now is that the government agency responsible for preserving competition is instead trying to take away our ability to further expand our low fares in these markets”

“I’m sad to say that our biggest obstacle to bringing more low fares and great service to the Northeast right now is the DOJ-the very government agency that should be making every effort to foster robust competition among airlines”

Name-calling, and accusing those who disagree with you as not even fit to do their jobs, is not “Inspiring Humanity.” Nor is it particularly wise, or engendering of good will, or a course of action that makes JetBlue’s claims and arguments seem particularly credible.

Individually and especially collectively, these issues are fatal to JetBlue’s proposed acquisition of Spirit. And they show just how drastically different the Frontier/Spirt merger is.

It is worth highlighting one additional factual data point, focusing on the difference between the two deals.

Remember Mr. Pomerantz? JetBlue’s antitrust lawyer in the special Q&A antitrust video? Mr. Pomerantz was asked the following question, via a slide—and provided the following answer, in full:24

“JetBlue is known for offering high quality service. They offer that service to business travelers, and they offer it to vacationers. Spirit and Frontier are known for offering basic service. And that difference in service is something that the DOJ and any court will consider in assessing this merger.”

Yes. That’s all he said. With all the polish, all the effort, and all the sleight of hand that JetBlue has attempted during this process, the best answer it can provide on this important point is that DOJ and any court will consider the different levels of service offered. And, of course, that means the different levels of prices offered and the demand stimulation which comes with Frontier/Spirit pricing, rather that JetBlue’s higher fares.

It seems clear to us, from this answer, that JetBlue itself thinks that the DOJ would prefer a Frontier-Spirit combination. And that, at least, is one thing that Frontier and JetBlue can agree on.

Citigroup Global Markets Inc. is serving as financial advisor and Latham & Watkins, LLP is serving as legal advisor to Frontier.

About Frontier Airlines

Frontier Airlines (Nasdaq: ULCC) is committed to “Low Fares Done Right.” Headquartered in Denver, Colorado, the company operates more than 110 A320 family aircraft and has among the largest A320neo family fleet in the U.S. The use of these aircraft, Frontier’s seating configuration, weight-saving tactics and baggage process have all contributed to Frontier’s continued ability to be the most fuel-efficient of all major U.S. carriers when measured by ASMs per fuel gallon consumed.

No Offer or Solicitation

This communication is for informational purposes only and is not intended to and does not constitute an offer to sell, or the solicitation of an offer to subscribe for or buy, or a solicitation of any vote or approval in any jurisdiction, nor shall there be any sale, issuance or transfer of securities in any jurisdiction in which such offer, sale or solicitation would be unlawful, prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended, and otherwise in accordance with applicable law.

Important Additional Information Will be Filed with the SEC

Frontier has filed with the Securities and Exchange Commission (“SEC”) a Registration Statement on Form S-4 in connection with the proposed transaction, that included a definitive Information Statement/Prospectus of Frontier and a definitive Proxy Statement of Spirit. The Form S-4 was declared effective on May 11, 2022 and the prospectus/proxy statement was first mailed to Spirit stockholders on May 11, 2022. Frontier and Spirit also plan to file other relevant documents with the SEC regarding the proposed transaction. INVESTORS AND STOCKHOLDERS ARE URGED TO READ THE REGISTRATION STATEMENT/ INFORMATION STATEMENT/ PROSPECTUS/ PROXY STATEMENT AND ANY OTHER RELEVANT DOCUMENTS TO BE FILED BY FRONTIER OR SPIRIT WITH THE SEC IN THEIR ENTIRETY CAREFULLY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT FRONTIER, SPIRIT, THE PROPOSED TRANSACTIONS AND RELATED MATTERS. Investors and stockholders are able to obtain free copies of the Registration Statement and the definitive Information Statement/Proxy Statement/Prospectus and other documents filed with the SEC by Frontier and Spirit through the website maintained by the SEC at www.sec.gov. In addition, investors and stockholders are able to obtain free copies of the information statement and the proxy statement and other documents filed with the SEC by Frontier and Spirit on Frontier’s Investor Relations website at https://ir.flyfrontier.com and on Spirit’s Investor Relations website at https://ir.spirit.com.

Participants in the Solicitation

Frontier and Spirit, and certain of their respective directors and executive officers, may be deemed to be participants in the solicitation of proxies in respect of the proposed transactions contemplated by the Merger Agreement. Information regarding Frontier’s directors and executive officers is contained in Frontier’s definitive proxy statement, which was filed with the SEC on April 13, 2022. Information regarding Spirit’s directors and executive officers is contained in Spirit’s definitive proxy statement, which was filed with the SEC on March 30, 2022.

Cautionary Statement Regarding Forward-Looking Information

Certain statements in this communication, including statements concerning Frontier, Spirit, the proposed transactions and other matters, should be considered forward-looking within the meaning of the Securities Act of 1933, as amended, the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on Frontier’s and Spirit’s current expectations and beliefs with respect to certain current and future events and anticipated financial and operating performance. Such forward-looking statements are and will be subject to many risks and uncertainties relating to Frontier’s and Spirit’s operations and business environment that may cause actual results to differ materially from any future results expressed or implied in such forward looking statements. Words such as “expects,” “will,” “plans,” “intends,” “anticipates,” “indicates,” “remains,” “believes,” “estimates,” “forecast,” “guidance,” “outlook,” “goals,” “targets” and other similar expressions are intended to identify forward-looking statements. Additionally, forward-looking statements include statements that do not relate solely to historical facts, such as statements which identify uncertainties or trends, discuss the possible future effects of current known trends or uncertainties, or which indicate that the future effects of known trends or uncertainties cannot be predicted, guaranteed, or assured. All forward-looking statements in this communication are based upon information available to Frontier and Spirit on the date of this communication. Frontier and Spirit undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events, changed circumstances, or otherwise, except as required by applicable law. All written and oral forward-looking statements concerning the Frontier merger or other matters addressed in this communication and attributable to Frontier, Spirit, or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this communication.

Actual results could differ materially from these forward-looking statements due to numerous factors including, without limitation, the following: the occurrence of any event, change or other circumstances that could give rise to the right of one or both of the parties to terminate the merger agreement; failure to obtain applicable regulatory or Spirit stockholder approval in a timely manner or otherwise and the potential financial consequences thereof; failure to satisfy other closing conditions to the proposed transactions; failure of the parties to consummate the transaction; risks that the new businesses will not be integrated successfully or that the combined companies will not realize estimated cost savings, value of certain tax assets, synergies and growth, or that such benefits may take longer to realize than expected; failure to realize anticipated benefits of the combined operations; risks relating to unanticipated costs of integration; demand for the combined company’s services; the growth, change and competitive landscape of the markets in which the combined company participates; expected seasonality trends; diversion of managements’ attention from ongoing business operations and opportunities; potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of the transaction; risks related to investor and rating agency perceptions of each of the parties and their respective business, operations, financial condition and the industry in which they operate; risks related to the potential impact of general economic, political and market factors on the companies or the proposed transaction; that Frontier’s cash and cash equivalents balances, together with the availability under certain credit facilities made available to Frontier and certain of its subsidiaries under its existing credit agreements, will be sufficient to fund Frontier’s operations including capital expenditures over the next 12 months; Frontier’s expectation that based on the information presently known to management, the potential liability related to Frontier’s current litigation will not have a material adverse effect on its financial condition, cash flows or results of operations; that the COVID-19 pandemic will continue to impact the businesses of the companies; ongoing and increase in costs related to IT network security; and other risks and uncertainties set forth from time to time under the sections captioned “Risk Factors” in Frontier’s and Spirit’s reports and other documents filed with the SEC from time to time, including their Annual Reports on Form 10-K and Quarterly Reports on Form 10-Q.

Contacts

Investor inquiries:

David Erdman

(720) 798-5886

david.erdman@flyfrontier.comMedia inquiries:

Jennifer F. de la Cruz

(720) 374-4207

jenniferf.delacruz@flyfrontier.comor

Joele Frank, Wilkinson Brimmer Katcher

Ed Trissel / Joseph Sala

(212) 355-4449

1 Interview with Robin Hayes, Chief Executive Officer, JetBlue Airways Corp., Bloomberg Markets (June 20, 2022), https://www.bloomberg.com/news/videos/2022-06-20/jetblue-ceo-access-to-second-permanent-heathrow-slot-video.

2 JetBlue Airways Corp., Analyst and Media Conference Call Transcript (Form DEF 14A) (Apr. 6, 2022), https://www.sec.gov/Archives/edgar/data/0001158463/000094787122000442/ss920339_dfan14a.htm.

3 JetBlue Airways Corp., Press Release, JetBlue CEO Robin Hayes Provides an Update on the Northeast Alliance and Action by the U.S. Department of Justice (DOJ) (Sept. 21, 2021), https://www.sec.gov/Archives/edgar/data/1158463/000115846321000080/ex991newsrelease-bluenote.htm.

4 JetBlue Airways Corp., Press Release, JetBlue Modifies Superior Offer After Consultation with Shareholders, (June 27, 2022), https://www.businesswire.com/news/home/20220627005782/en/JetBlue-Modifies-Superior-Offer-After-Consultation-with-Shareholders.

5 JetBlue Airways Corp., Interview with Glenn Pomerantz, Attorney Advisor, https://jetblueoffersmore.com/regulatory-confidence/.

6 JetBlue Airways Corp., Press Release, JetBlue Comments on Glass Lewis Report (June 3, 2022), https://www.sec.gov/Archives/edgar/data/0001158463/000119312522167395/d365445ddfan14a.htm.

7 Def.’s Mem. Supp. Mot. to Dismiss at 2, U.S., et al. v. American Airlines Group Inc., et. al., 2021 WL 8776286 (D. Mass. Nov. 22, 2021) (emphasis added).

8 David Slotnick, Skepticism on Wall Street as details emerge on JetBlue’s bid for Spirit, The Points Guy (Apr. 6, 2022), https://thepointsguy.com/news/spirit-airlines-jetblue-wall-street-skepticism/; see also Jack Hough, The Best Airline Bet Might Be the One That Owns An Oil Refinery, Barron’s (Apr. 8, 2022), https://www.barrons.com/articles/jetblue-spirit-delta-51649456037 (“The premise for this whole merger…just eliminates 10% to 11% of all seats right out the door immediately…”).

9 Interview with Robin Hayes, supra note 1.

10 JetBlue Airways Corp., Investor Presentation at 19 (Form DEF 14A) (Apr. 6, 2022), https://www.sec.gov/Archives/edgar/data/1158463/000094787122000441/ss917756_dfan14a.htm.

11 Seth Miller, A JetBlue-Spirit merger almost certainly means higher fares, Paxex.Aero (Apr. 6, 2022), https://paxex.aero/jetblue-spirt-merger-higher-fares; see also Dawn Gilbertson, The battle for Spirit Airlines just got more interesting: Airline says it will entertain JetBlue's $3.6 billion offer, USA Today (Apr. 7, 2022), https://www.usatoday.com/story/travel/airline-news/2022/04/07/jetblue-spirit-bid-budget-airline-weighs-offer/9507114002/ (“If the deal went through, JetBlue said Spirit would be absorbed into JetBlue, with seats taken out of its planes to conform with JetBlue's roomier configuration. Analysts say that pricey plane conversion can't be done without raising fares. Already, JetBlue's fares are higher than Spirit's on some competing routes. For a June trip from Fort Lauderdale to New York, Spirit's cheapest fare is $156, compared with $289 on JetBlue. The latter is for a JetBlue basic economy ticket”).

12 JetBlue Airways Corp., Analyst and Media Conference Call Transcript (Form DEF 14A) (Apr. 6, 2022), https://www.sec.gov/Archives/edgar/data/0001158463/000094787122000442/ss920339_dfan14a.htm.

13 JetBlue Airways Corp., Interview with Robin Hayes, Chief Executive Officer, and Scott H Group, Wolfe Research LLC, at Wolfe Research, LLC’s 15th Annual Global Transportation & Industrials Conference (May 26, 2022), https://www.sec.gov/Archives/edgar/data/1158463/000119312522162303/d304700ddfan14a.htm.

14 JetBlue’s Press Release, supra note 3.

15 JetBlue Airways Corp., Press Release, JetBlue Urges Spirit Shareholders to Protect Their Interests and ‘Vote No’ on Frontier Transaction at Upcoming Spirit Special Meeting (May, 16, 2022), https://www.sec.gov/Archives/edgar/data/1158463/000119312522150775/d332868dex99a5a.htm.

16 JetBlue Airways Corp., Investor Presentation at 7 (Form DEF 14A) (June 27, 2022), https://www.sec.gov/Archives/edgar/data/1158463/000119312522169027/d355394ddfan14a.htm..

17 Friday Flyer: the Jet Blue Effect?, Wolfe Research (Apr. 8, 2022).

18 See JetBlue – Spirit Merger: v2.0, deal day observations, tactical trade idea, J.P. Morgan (Apr. 6, 2022), https://markets.jpmorgan.com/research/email/-usu4g0c/Dn5tdPGdsl7OQVkMTL6Hiw/GPS-4054656-0.

19 Joanna Geraghty, President and COO JetBlue Airways, Letter to crewmembers (Sept. 28, 2018), http://blog.jetblue.com/where-can-we-inspire-humanity-next/.

20 Brian Pascus, JetBlue is launching a basic economy fair to help it compete with Delta, United, and American, Business Insider (Sept. 28, 2018) https://www.businessinsider.com/jetblue-to-add-basic-economy-fare-like-delta-american-and-united-2018-9.

21 Andrea Sachs, No-frill fares are all the rage. Even JetBlue will start offering basic economy., Washington Post (Oct. 10, 2018) https://www.washingtonpost.com/lifestyle/travel/no-frill-fares-are-all-the-rage-even-jetblue-will-start-offering-basic-economy/2018/10/09/b409fdfc-cb0a-11e8-a3e6-44daa3d35ede_story.html.

22 JetBlue Airways Corp., Investor Presentation at 31 (Form DEF 14A) (June 7, 2022), https://www.sec.gov/Archives/edgar/data/1158463/000119312522169027/d355394ddfan14a.htm.

23 JetBlue’s Press Release, supra note 3.

24 Interview with Glenn Pomerantz, supra note 5.Photos are available at:

https://www.globenewswire.com/NewsRoom/AttachmentNg/a908aa30-1c29-4675-b20b-9a672d5595a6

https://www.globenewswire.com/NewsRoom/AttachmentNg/68b0d115-4ae8-4532-920b-7de0b729317c

https://www.globenewswire.com/NewsRoom/AttachmentNg/4c9f6c60-41c1-4318-95d1-694c76d4cf14

https://www.globenewswire.com/NewsRoom/AttachmentNg/4499fd7a-0dc1-412e-950e-fe0567d0e605

https://www.globenewswire.com/NewsRoom/AttachmentNg/5202791a-3eea-4098-94c5-74e152b2f697

https://www.globenewswire.com/NewsRoom/AttachmentNg/63d3ba32-66a0-4f26-a445-6a91f881fc09

https://www.globenewswire.com/NewsRoom/AttachmentNg/cb399c5a-560a-4c35-9070-fff6279064f2

https://www.globenewswire.com/NewsRoom/AttachmentNg/52efdbce-63ff-4acd-851d-a5c367671f39

https://www.globenewswire.com/NewsRoom/AttachmentNg/eb6864ee-bb6a-4c24-abf1-e365d10c75d8

https://www.globenewswire.com/NewsRoom/AttachmentNg/60959f91-ee38-41e2-be84-b9faa07e855d

https://www.globenewswire.com/NewsRoom/AttachmentNg/3a6d2208-f4f9-4adf-a781-9652af24e73b

Photo 1

Photo 1

Photo 2

Photo 2

Photo 3

Photo 3

Photo 4

Photo 4

Photo 5

Photo 5

Photo 5

Photo 5

Photo 6

Photo 6

Photo 7

Photo 7

Photo 8

Photo 8

Photo 9

Photo 9

Photo 10

Photo 10

Photo 5

Photo 5

Picture 11

Picture 11

Photo 1

Photo 1